Why Economists Keep Predicting Dubai Will Collapse

The city built on theater, not oil. And why Western models can't explain what actually holds it together.

When Sheikh Rashid discovered oil 15 miles offshore in 1966, he had a problem: nobody could see it. So he loaded crude onto a barge, towed it into the Creek, and pumped it into a sand embankment along the shore.

Oil appeared to flow from beneath the city itself. It was pure theater. Dubai never actually had much oil. Abu Dhabi holds 94% of the UAE’s proven reserves. Dubai’s were modest and started declining by the 1990s. Today, oil contributes less than 1% of Dubai’s GDP.

And yet for 30 years, the same Western analysts have kept predicting its collapse. The predictions use economic vocabulary, cite real conditional risks, and arrive at the same conclusion every time: unsustainable.

But strip away the models and what you find isn't economics. It's a story about how wealth is supposed to be earned, who deserves to have it, and what should happen to those who got it wrong.

Dubai keeps violating that story. The predictions keep coming anyway.

The First Thing the Predictions Have to Ignore

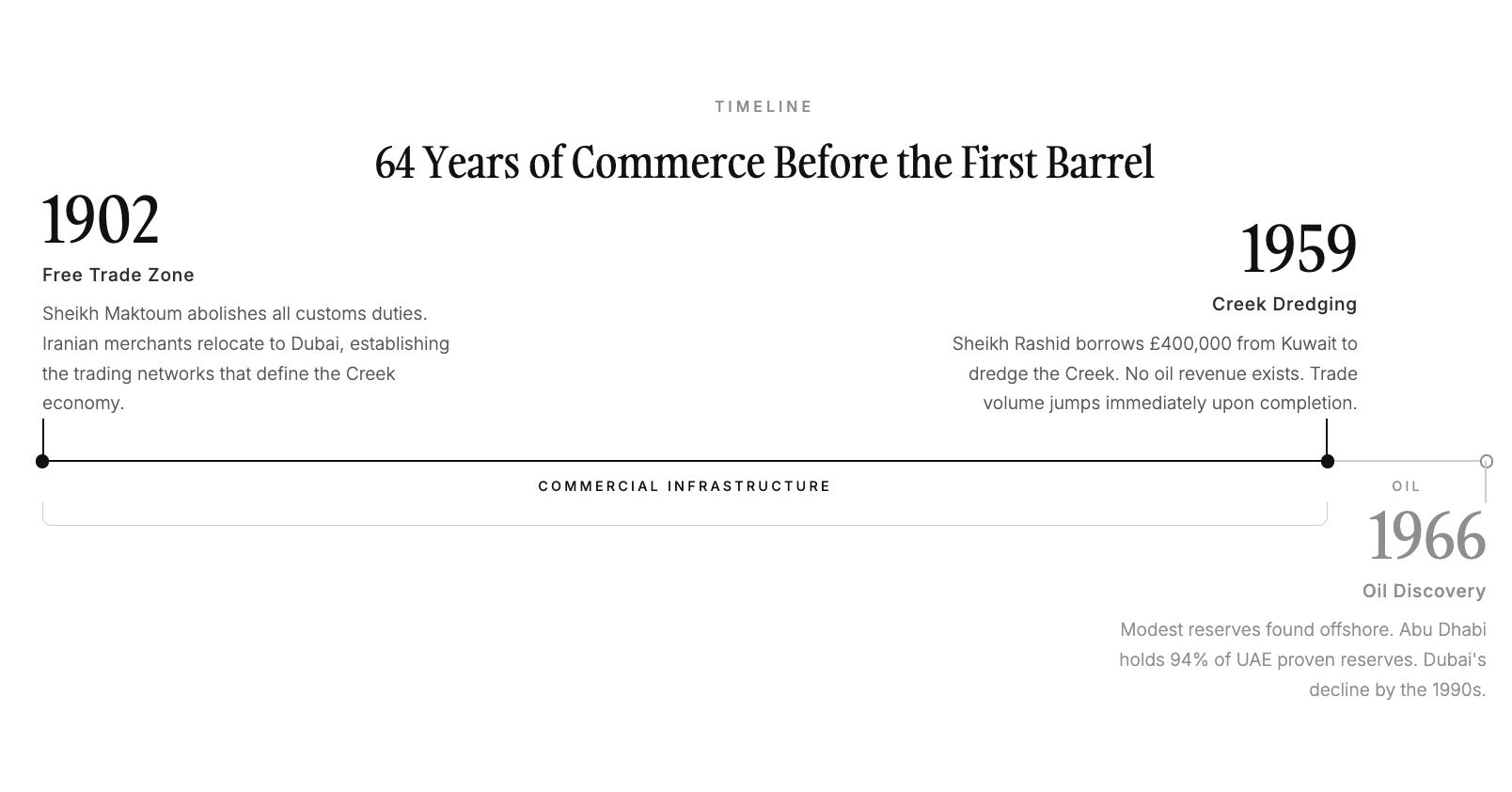

To sustain the story that Dubai is a petrostate waiting to implode, you have to skip past sixty-four years of commercial history that precedes the oil.

In 1902, Sheikh Maktoum bin Hasher abolished all customs duties on imports. No tariffs. No processing fees. An open door for anyone who wanted to trade through Dubai’s Creek. When Iran raised its own customs duties a year later, a wave of Iranian merchants relocated from Bandar Lengeh, bringing their families, their trading networks, and their architectural traditions. The coral-stone houses with wind towers that tourists photograph in old Dubai today were built by those Iranian settlers.

By 1949, the pearl industry had collapsed (Kokichi Mikimoto’s cultured pearls had killed the Gulf’s wild-catch market), and Dubai was in desperate shape. People were eating leaves, locusts, and a spiny desert lizard called dhub that tastes like chicken if you’re generous and like sand if you’re honest. The town had maybe 20,000 people and a creek so silted up that large dhows couldn’t enter.

Sheikh Rashid, who took power formally in 1958 but was running things well before, commissioned a British engineering firm to dredge the Creek. Their 1955 feasibility report contains a line of wonderful British understatement: “No records exist of any recent civil engineering works of any magnitude in Dubai and this, coupled with the isolated position of the country, make accurate estimation of costs difficult.” The price tag was £388,000, extraordinary for a town with no oil revenue. He scraped together £200,000 from a local bank and secured a £400,000 loan from Kuwait. When the dredging finished, ships of 500 tonnes could enter. Trade volume jumped immediately.

Edward Henderson, a British oil company representative, described a place where business worth millions was conducted with a wink and a nod, where an expanding town was operating under oil boom conditions fifteen years before any oil was actually discovered. Henderson wrote a line that reads differently in hindsight: “Goodness, what will he be like if he does find oil?”

The free trade zone in 1902. The infrastructure investment in 1959. The oil discovery in 1966. Dubai didn’t need oil to understand commerce. It needed oil to scale what it already knew.

What “Unearned” Actually Means

Why do the collapse predictions keep coming? Because Dubai violates a particular story about how wealth becomes legitimate.

The Western economic narrative is built on a template: labor, sacrifice, deferred gratification, productive struggle. This story has enormous power. It motivates. It organizes. It gives meaning to decades of effort. When a country satisfies the template (Japan’s postwar recovery, Singapore’s ascent from poverty, South Korea’s industrialization), Western analysts call it a miracle and admire it. When a country violates the template, they reach for words like “unsustainable” and “distortion.”

The Gulf violates that narrative. A commodity the world needs sits beneath their ground, and the world pays for it at scale. When wealth appears without the expected suffering, it triggers something that looks like analysis but functions like defense.

People predict collapse. They use economic vocabulary. They cite conditional mechanisms (Dutch Disease, resource curse, rentier effects) that describe real risks under specific conditions. But in ordinary conversation, the conditions drop away and the conclusion hardens: this wealth is unearned, therefore it is temporary.

That smuggles “deserved” into “durable.” It treats moral legitimacy and structural resilience as the same thing, when they are entirely separate questions.

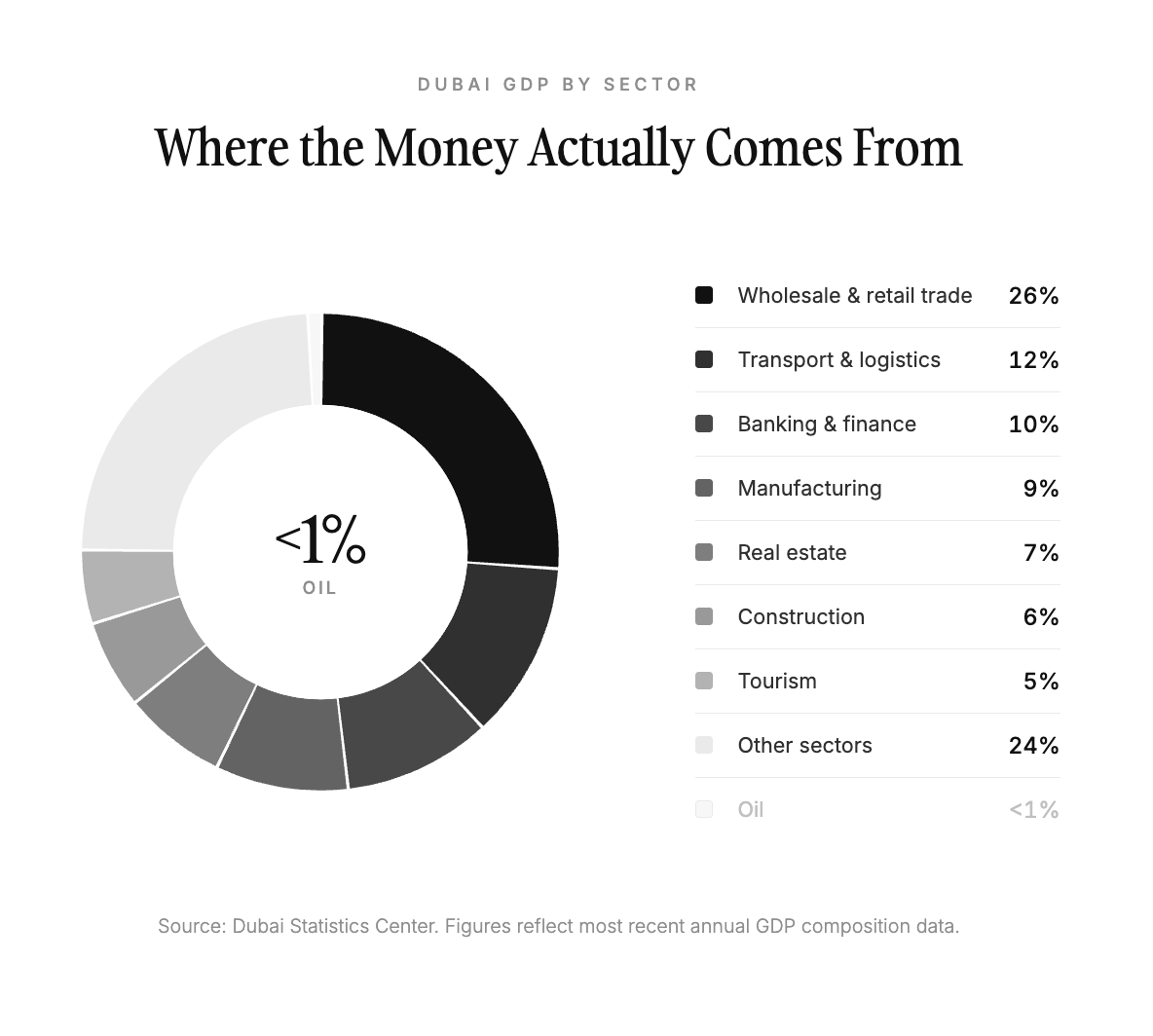

This framing persists even when the data contradicts it. Dubai’s economy runs on wholesale and retail trade (26%), transport and logistics (12%), banking and finance (10%), manufacturing (9%), real estate (7%), construction (6%), and tourism (5%). No single sector dominates. By most measures, it is more diversified than many Western cities of comparable size. And still the analysis defaults to “petrostate.”

A Framework That Broke Inside the Academy

The intellectual scaffolding behind the predictions has a name: rentier state theory. In 1970, Hossein Mahdavy coined the concept to describe pre-revolutionary Iran, a state funded by resource rents from foreign buyers rather than by taxing its own citizens. Beblawi and Luciani formalized it in 1987, arguing that rentier wealth breaks from the “work-reward system” because it comes from “chance or situation” rather than productivity. That sounds like a neutral observation. It is also a value judgment embedded in an economic model. The “work-reward system” is treated as the baseline. Deviation from it becomes pathology.

The critics within the discipline have been saying this for years. Emilie Rutledge, publishing in the OPEC Energy Review in 2017, pointed out that the contemporary notion of rent as “essentially constituting unearned and thus unwarranted income” is divorced from the more accurate idea of ground rent as a legitimate charge for extracting depletable sovereign resources. Scholars treat oil revenue differently from coffee or cocoa revenue, and that difference has nothing to do with economics.

Ozyavuz and Schmid, writing for the French Institute of International Relations in 2015, named the problem directly: “This is where the hint of Orientalism that is sometimes evoked surfaces... analysis of rent in the Middle East appeared to support cultural prejudices.” They called classical rentier state theory “implicitly culturalist, betraying the energy-scarce West’s unease concerning the unequal distribution of energy resources.”

Even Luciani, one of the two scholars who formalized the original theory, eventually distanced himself: “It has never been my understanding that the rentier state paradigm should be either the sole or the overwhelming tool of interpretation.” Among Gulf specialists, by 2019, the original theory appeared “more often as a foil than as a bedrock theoretical perspective.” The framework’s own architects walked away from it.

Outside the academy, in Western media and popular commentary, the theory calcified into a genre. Martin Peretz, then editor-in-chief of The New Republic, wrote in 2008 that Dubai was “a Potemkin village, a house of cards, a mirage” and that it would collapse “soon.” The trigger changed over the decades. The conclusion never did.

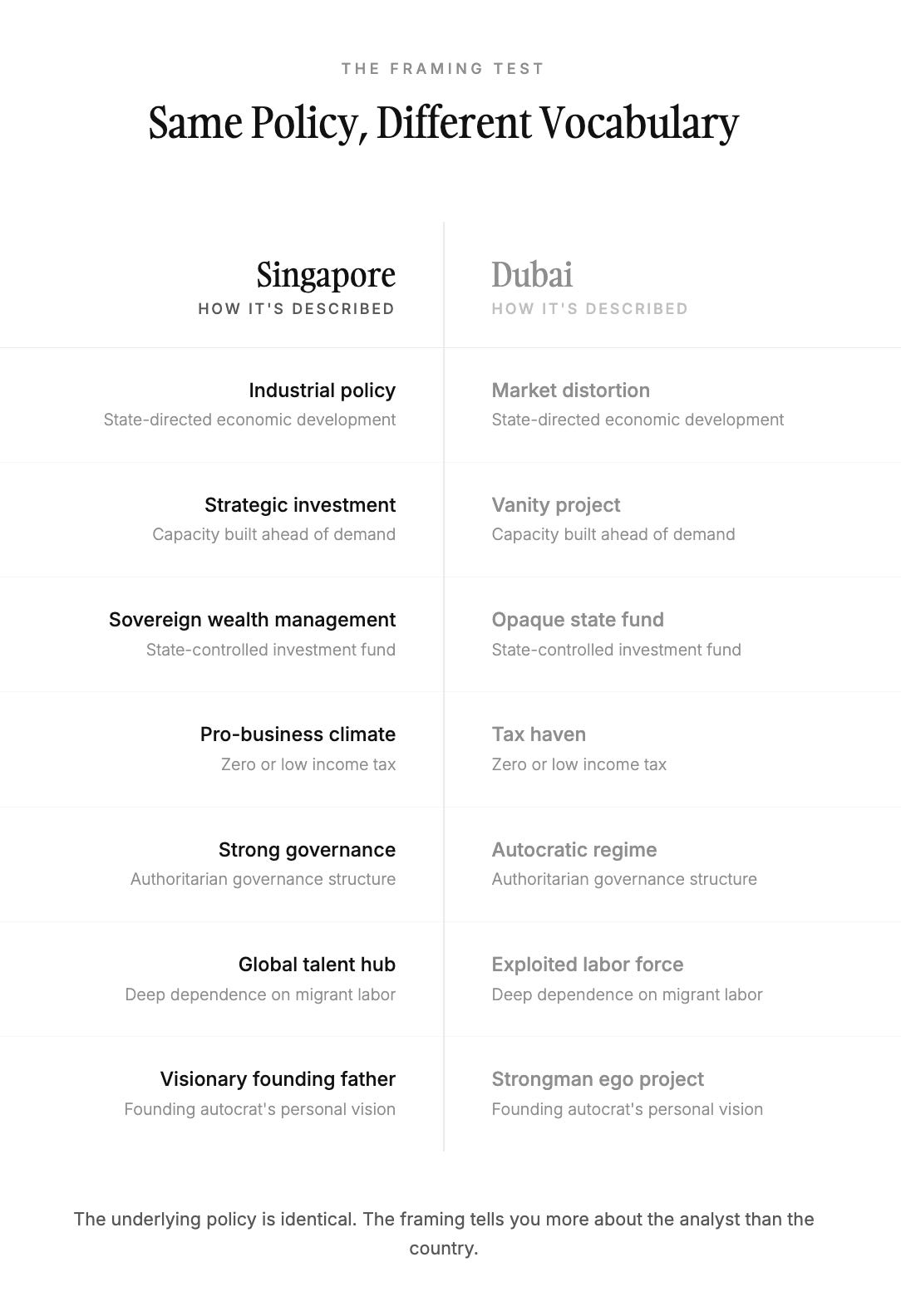

The comparison that exposes this most clearly is Singapore. Singapore and Dubai share state-directed economic development, authoritarian governance structures, sovereign wealth funds, zero or low income taxes, a deliberate strategy of becoming a hub, deep dependence on migrant labor, and a founding autocrat whose personal vision drove the whole project.

When Singapore intervenes in markets, it’s called competence. When Gulf states do the same thing, it’s called distortion. Both are state-directed capital. The difference in how they’re discussed tells you more about the person doing the analysis than the country being analyzed.

The 2008 Test

The financial crisis gave the skeptics what looked like vindication.

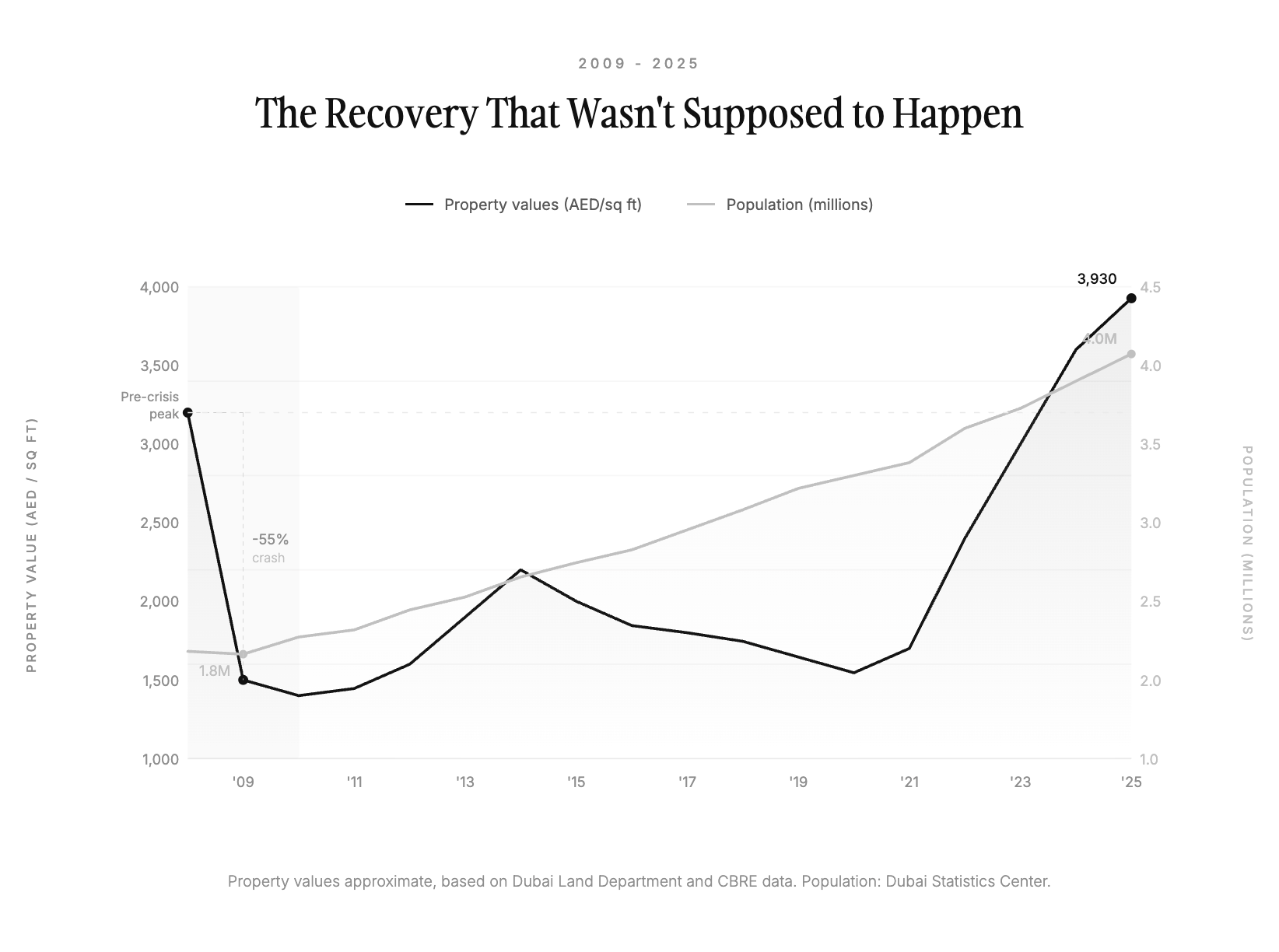

Dubai had borrowed roughly $80 billion during a four-year construction boom. Property prices had quadrupled between 2002 and 2008. The Atlantis Hotel on Palm Jumeirah opened on November 24, 2008, with a $24 million launch party featuring a Kylie Minogue concert and fireworks visible from space. This was less than two months after Lehman Brothers collapsed.

By early 2009, property prices in some areas had fallen 50-60%. On November 25, 2009, Dubai World announced it would seek a six-month standstill on $59 billion in debt repayments. European stocks dropped 3%. The Dow fell 155 points. Bank of America warned this could “escalate into a major sovereign default problem, which would then resonate across global emerging markets in the same way that Argentina did in the early 2000s or Russia in the late 1990s.”

For the collapse crowd, this was the ending they had been writing in their heads for years.

Abu Dhabi stepped in with approximately $25 billion in support. The Burj Khalifa opened in January 2010, renamed from “Burj Dubai” at the ceremony to honor Sheikh Khalifa bin Zayed of Abu Dhabi. Everyone understood what the name change meant. Ten months after opening, 825 of its 900 apartments sat empty. Coverage was gleeful. The world’s tallest building as monument to hubris.

Then something happened that the predictions couldn’t accommodate: Dubai recovered.

Dubai World restructured $23.5 billion in debt by May 2010. Nakheel repaid its restructured obligations ahead of schedule and posted AED 860 million in profit by year-end 2010. By October 2012, Burj Khalifa occupancy hit 80%. By 2024-25, it was running between 85 and 90 percent, with capital values reaching AED 3,930 per square foot (a 60% increase since 2021).

Dubai’s population doubled from 1.8 million in 2009 to 4 million by August 2025. Property transactions hit 205,100 residential sales worth $147 billion in 2025. The city attracted more greenfield FDI projects than any other city on earth for the fourth consecutive year.

Consider that the same pattern repeated in miniature with Emirates airline. In 1985, when Gulf Air cut service to Dubai, Sheikh Mohammed started a national airline from scratch: five months to launch, $10 million in seed funding, two planes wet-leased from Pakistan International Airlines. First year: 260,000 passengers and 10,000 tons of freight. Gulf Air’s profits dropped 56%. Analysts called it vanity.

By fiscal year 2024-25, the Emirates Group posted $34.9 billion in revenue and $6.2 billion in profit on a fleet of 260 aircraft. It is the most profitable airline in the world. Jebel Ali Port, dismissed as overkill for a small Gulf emirate, now handles 15.5 million TEUs annually, ahead of Rotterdam and Hong Kong. Capacity built ahead of demand reads as hubris to forecasters who assume demand is fixed. It reads as strategy to anyone who has watched Dubai for more than one cycle.

Mohammed Alabbar, chairman of Emaar Properties, said: “Crises come and go. And cities move on.”

The Story That Doesn’t Update

Sheikh Rashid reportedly told an advisor: “My grandfather rode a camel, my father rode a camel, I drive a Mercedes, my son drives a Land Rover, his son will drive a Land Rover, but his son will ride a camel.” He saw the timeline. The urgency that built Dubai came from that awareness, not from Western op-eds. The response to that urgency was to convert the windfall, relentlessly, into infrastructure, connectivity, and institutional capacity that would outlast the resource.

The real risks exist: concentrated decision-making in a single ruling family, dependence on Abu Dhabi as a financial backstop (as 2008 proved), and a structural reliance on migrant labor with limited political voice. A properly calibrated framework would interrogate those vulnerabilities. Instead, the predictions keep defaulting to “oil will run out” for a city that already ran past oil and kept growing.

The crisis was real. The recovery wasn’t supposed to be. The predictions have been wrong for thirty years because they were never really about economics. They were about sustaining a story of how wealth is supposed to work. And stories, unlike economic models, don’t update when the data comes in.