The Crisis That Broke Thailand Forever

A 49-story ghost tower, a currency that lost half its value, and a national psyche that never fully recovered.

In downtown Bangkok, a 49-story luxury tower stands completely empty. It has been empty for 27 years.

The Sathorn Unique was 80% complete when Thailand’s currency lost half its value in six months, GDP contracted 10.5% in a single year, and 56 of 91 finance companies were permanently shut down.

The developer’s son refused to declare bankruptcy. He wanted to repay every original buyer in full. That never happened. The tower survived the 2025 Myanmar earthquake that shook Bangkok. It became the set of a Thai horror film. It hosted a seminar on the 20th anniversary of the crisis that killed it.

It is, by any measure, the most haunting monument to a financial crisis anywhere in the world. The crisis ended decades ago. The psychology it installed never did.

The first time I went to Bangkok, in August 2023, I couldn’t square what I was seeing with what I thought I knew. The people were visibly sharp. The youth dressed like they’d walked off a Seoul street and spoke English with an ease I hadn’t expected.

One Bangkok, the $3.9 billion mixed-use district designed by the architects behind the Burj Khalifa, was rising in the center of the city. ICONSIAM, a $1.65 billion riverside mega-mall, housed an indoor floating market representing all 77 Thai provinces alongside Louis Vuitton and Chanel.

I’ve been going back regularly since then, and the feeling has only deepened. Thailand is full of people who should be living in a country that works better than it does.

The standard story about developing economies is that the bottleneck is human capital: the workforce is underskilled, the educational pipeline is broken, the culture doesn’t support innovation. Thailand inverts every one of those assumptions and still can’t break through. Between 2015 and 2024, Thailand averaged 1.9% GDP growth. Vietnam posted 7%. Indonesia managed 5%. Malaysia came in between 4 and 5%. Thailand fell from second to fifth among ASEAN economies for foreign direct investment between 2010 and 2022.

Over 3,500 factories shut between 2021 and 2024, with 51,500 workers losing their jobs in the twelve months through June 2024 alone (an 80% year-on-year increase). Subaru ceased all assembly at its Lat Krabang plant after production collapsed to 344 units in four months.

Suzuki announced closure of its Rayong factory by end of 2025. Samsung moved smartphone production to Vietnam years earlier, where its six factories now account for over 50% of the company’s global smartphone output and generate roughly 30% of Samsung’s total revenue. The consumer side is cracking alongside manufacturing: auto loan non-performing loans surged 32% year-on-year, car leasing NPLs hit 27.25% in Q4 2024, and commercial bank lending has contracted for four consecutive quarters, the longest contraction in over 20 years.

The numbers tell you what happened. They don’t tell you why. The answer is a structural trap with interlocking parts: a crisis that installed permanent caution, a concentration of wealth that was strengthened by that caution, and a demographic collapse driven by the resulting lack of opportunity. Each piece makes the others harder to fix, and the combined weight makes the trap politically unsurvivable: no leader lasts long enough to coordinate an escape.

The Psychology That Never Left

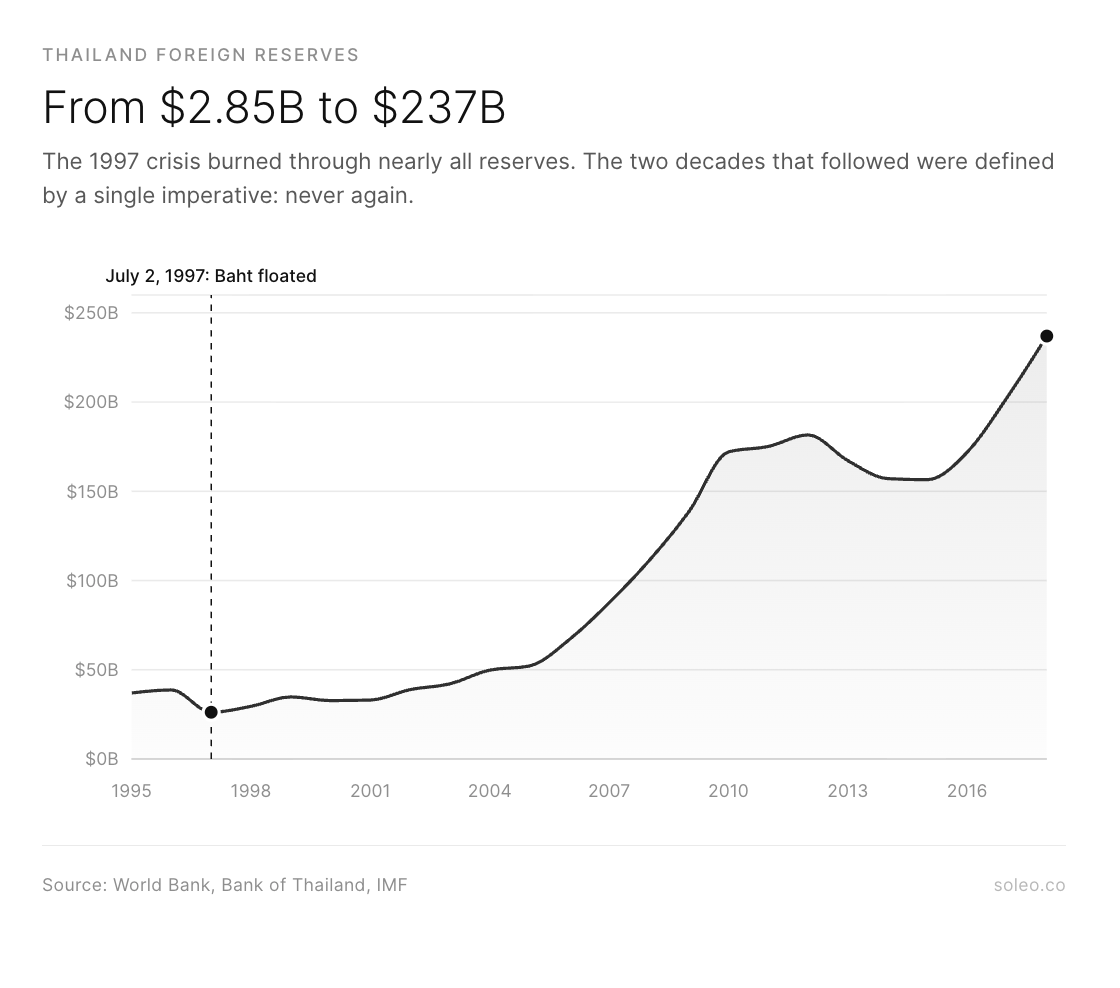

On July 2, 1997, the Thai baht was unpegged from the dollar after 14 years at a rate of 25:1. By January 1998, it had plunged to 56. Of the $38.7 billion in foreign reserves, only $2.85 billion remained. The IMF assembled a $17.2 billion rescue package. Over 300 high-rise projects were abandoned mid-construction across Bangkok. U.S. diplomat Marie Therese Huhtala recalled people pulling their kids out of school, executives losing everything, wealthy families selling furs and Mercedes at fire-sale prices.

The Bank of Thailand itself acknowledges the crisis left “remaining scars.” These manifest as institutional risk aversion of an intensity that is difficult to overstate. Foreign reserves were rebuilt from $2.85 billion to over $237 billion by 2018. Banking regulation became among the strictest in the region, with capital adequacy ratios at 17.8% and loan-loss reserves at 162% of required amounts. Corporate investment has been persistently weak since 1997.

Here is the frame that got installed: caution above all else. Safe export-oriented manufacturing. Tourism. Strategies that generate foreign exchange without the vulnerability of foreign borrowing. These were rational choices. They were also the choices of a country that would never again bet on itself the way it had in the late 1980s, when Thailand’s economy was growing at over 9% annually, the highest rate of any country on Earth.

The aspiration was set in that era. The caution was set by what came after. Both are still running simultaneously, and neither can overwrite the other. That tension defines modern Thailand more than any single policy failure.

And the caution didn’t just shape policy. It shaped who won.

Where the Money Sits, and Where It Doesn’t

If the 1997 crisis installed the psychology, the psychology installed the structure.

A banking system that will only lend to proven balance sheets lends to conglomerates. A regulatory system terrified of destabilizing the economy doesn’t challenge incumbents. An investment climate that only funds what’s already validated funds the people who already own everything.

Thailand didn’t develop extreme wealth concentration because a few families seized power. It developed extreme wealth concentration because the caution frame, applied consistently for 27 years, has a natural output: whoever was big enough to survive 1997 absorbed everything that came after.

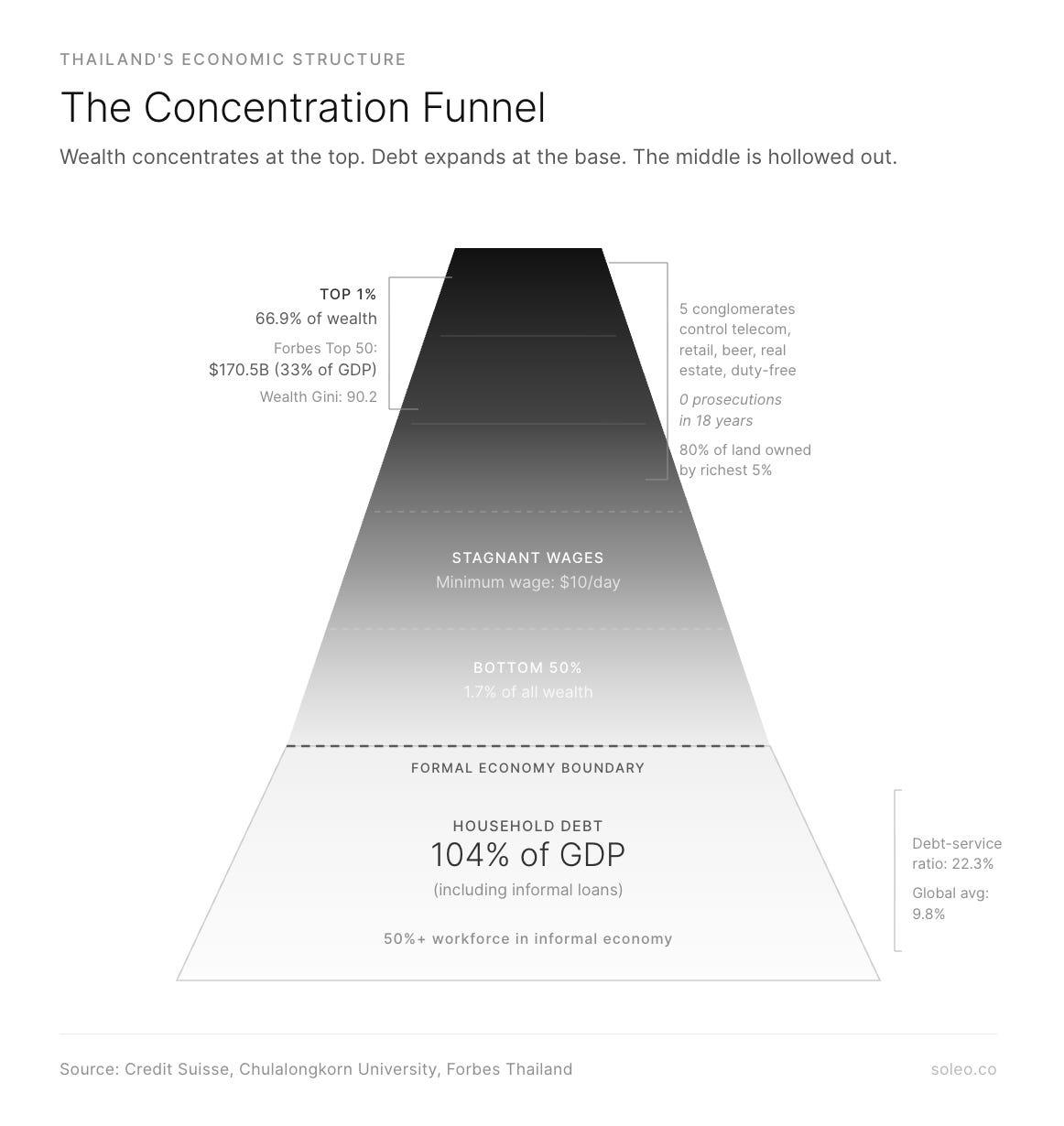

Credit Suisse’s 2018 Global Wealth Databook ranked Thailand the most unequal country in the world among 40 nations surveyed. The richest 1% controlled 66.9% of all wealth. The bottom 50% held 1.7%. But the numbers matter less than the mechanism.

CP Group was forced to sell Lotus during the 1997 crisis. Then it bought everything back (Makro in 2013, Tesco Lotus for $10.6 billion in 2020) at moments when smaller competitors couldn’t finance operations. Today, CP Group controls 14,000 7-Eleven stores, Thailand’s largest telecom operator, and one of the world’s largest agribusiness operations. TCC Groutp controls Thai Beverage, massive real estate holdings, and is the developer behind One Bangkok. Together with Boon Rawd Brewery, TCC controls over 90% of Thailand’s beer market. King Power holds a near-total monopoly on duty-free retail. The combined wealth of Forbes Thailand’s top 50 reached $170.5 billion in 2025, roughly 33% of the country’s entire GDP.

Thailand’s 1999 Trade Competition Act yielded zero prosecutions in its first 17 years. When the True-DTAC telecom merger reduced the mobile market from three to two major players in 2023, the deal proceeded without resistance. This wasn’t corruption in the traditional sense; it was the caution frame working exactly as designed: don’t disrupt what’s functioning, don’t risk instability, don’t bet on an outcome you can’t guarantee.

Every subsequent downturn repeated the cycle. COVID was the most recent iteration: the big conglomerates were described as “among the few cashed-up Thai buyers” for distressed bank portfolios. The crisis that broke the middle class made the conglomerates stronger. Then the caution that followed the crisis made them permanent.

A Country Aging Without Getting Rich

The detail that reframes everything is the birth rate.

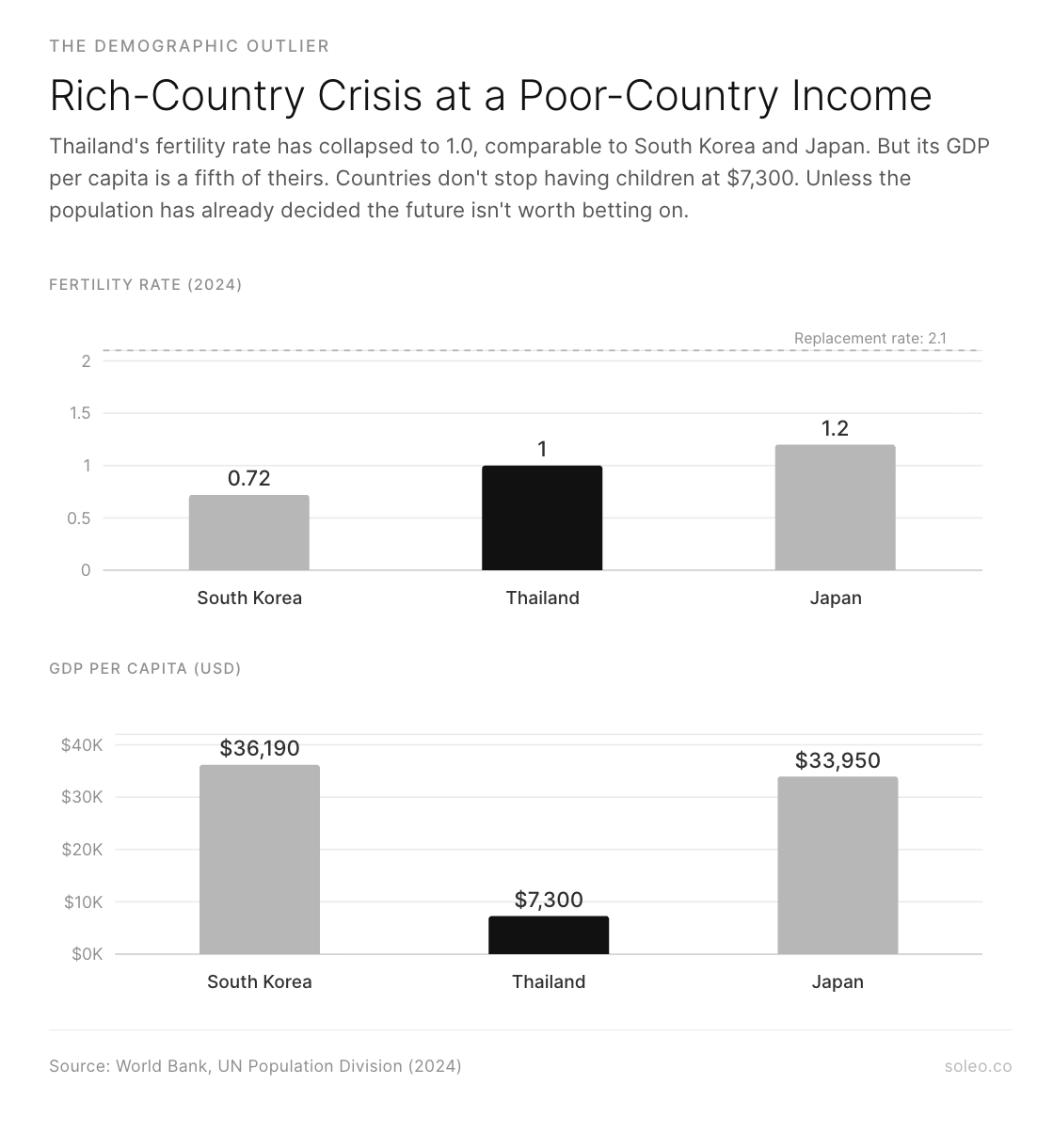

Thailand’s total fertility rate fell to 1.0 in 2024. Lower than Japan’s 1.2. Approaching South Korea’s record-breaking 0.72. But South Korea’s GDP per capita is five times higher, at $36,000 versus Thailand’s $7,300. Thailand is the only Southeast Asian country the UN classifies among nations with declining birth rates, a group that otherwise consists entirely of high-income, developed economies.

In 2024, Thailand recorded 462,240 births versus 571,646 deaths. The first time births fell below 500,000 since 1949. The fourth consecutive year deaths exceeded births. Thailand’s median age of 40.8 matches the United Kingdom’s. The ASEAN average is 29. By 2050, one in three Thais will be over 60, and the working-age population will shrink from 43.2 million to 36.5 million.

This demolishes the standard assumption that birth-rate collapse is purely about wealth. Thailand’s plunge below replacement fertility began in 1991, driven by an extraordinarily successful 1970s family planning program that cut population growth from 3.1% to 0.4%. But the continued decline, a survey found only 35.8% of fertile Thai adults plan to have children, is driven by something harder to measure: the sense that the future doesn’t hold enough promise to invest in.

The conglomerate structure and the demographic decline reinforce each other: young people opt out because the economy offers them no path forward, and their departure further concentrates the domestic market in the hands of the incumbents who already dominate it. The “Let’s Move Abroad” Facebook group, created in May 2021, attracted nearly 1.1 million members almost immediately. In a country of 72 million, that is a mass expression of generational despair.

Thailand produces 400,000 to 500,000 university graduates annually, fewer than half of whom find immediate formal employment. Starting salaries hover around 15,000 to 20,000 baht per month ($420 to $560). A single BTS/MRT fare of 39.50 baht represents 11% of the daily minimum wage, the highest proportion in Asia. Bangkok earned UNESCO Creative City of Design designation in 2019. The 2024 film How to Make Millions Before Grandma Dies was an international breakout. The creative talent is unmistakable. The economic infrastructure to support it is not.

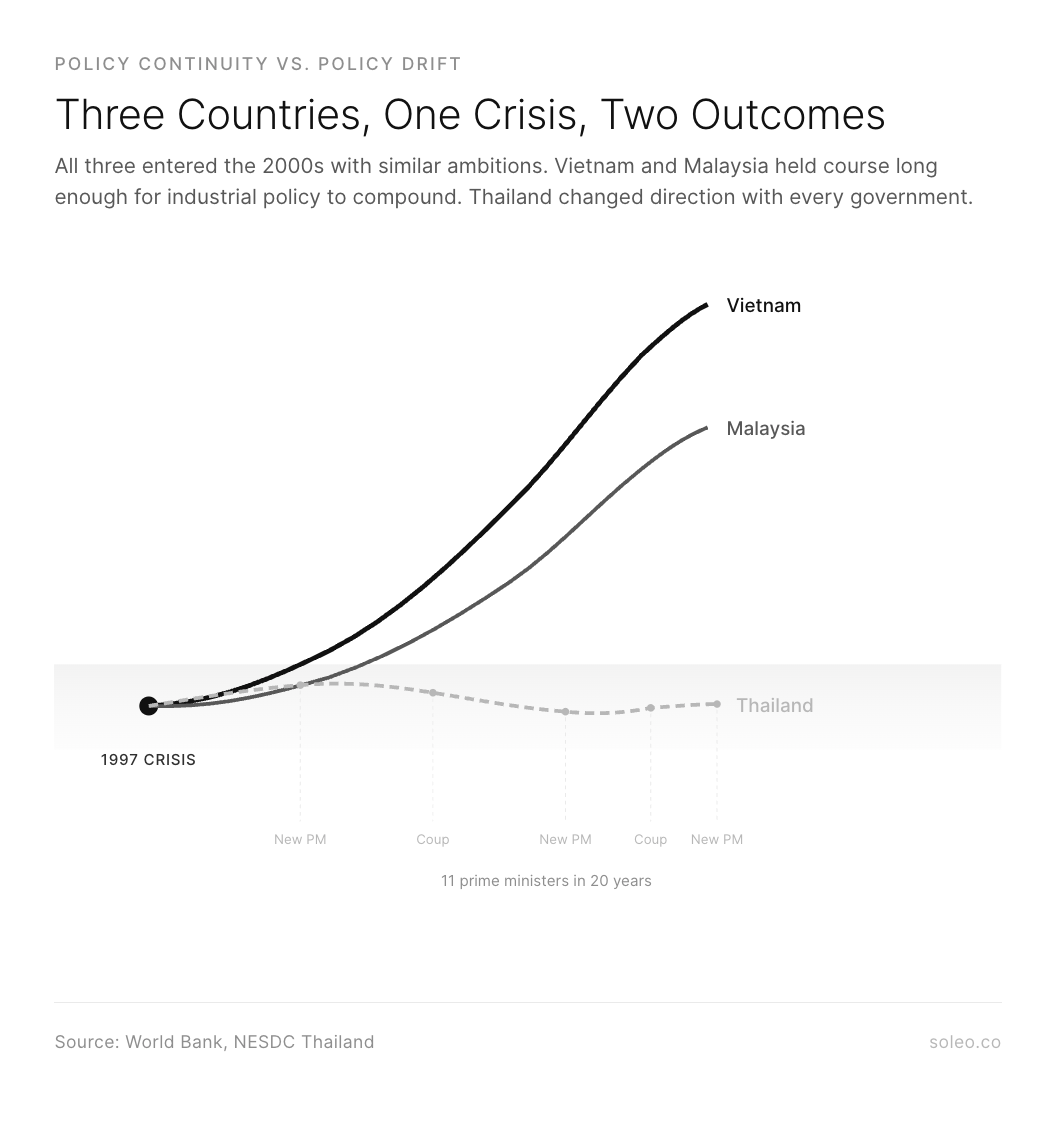

Breaking free would require coordinated industrial policy sustained over decades. An economy this rigid, a demographic clock this advanced, a debt burden this heavy: the structural conditions make that coordination almost impossible. Thailand has had 11 prime ministers in 20 years, not because its politics are uniquely dysfunctional in isolation, but because the trap itself is politically unsurvivable. No leader holds power long enough to execute a strategy that takes a generation to pay off.

Why Others Pulled Away

Vietnam and Malaysia clarify what escape looks like.

Samsung’s Vietnamese supplier base grew from 25 enterprises in 2014 to 257 by 2022, a tenfold increase in local supply chain development. Vietnam secured a tariff deal with the United States. Intel committed $7 billion to expand advanced chip packaging in Penang, making it Intel’s largest global production base. Malaysia’s five economic corridors have collectively attracted $162 billion in cumulative investment. The Johor-Singapore Special Economic Zone is becoming a hyperscale data center hub.

What separates these countries from Thailand is policy continuity. Vietnam’s system provides consistent, decades-long investment-friendly policy. Malaysia operates on five-year development plans with dedicated statutory authorities for each economic corridor that function regardless of government changes, even through Malaysia’s own turbulence of three prime ministers between 2018 and 2022. These countries could make long-horizon bets and hold them.

Thailand, with its economic rigidity generating constant political churn, could not. The World Economic Forum found that business executives ranked leadership turnover as the single most problematic factor for doing business in Thailand. The signature digital wallet stimulus was indefinitely postponed in May 2025 with 157 billion baht reallocated after yet another transition in leadership.

Thailand has been middle-income for 37 years. World Bank simulations suggest it will likely remain so past 2050 under current trends. South Korea, starting from a similar GDP per capita in 1960, broke through in under three decades by investing heavily in domestic innovation, R&D, and education. Thailand chose the safe path and has been rewarded with safety and nothing more.

Every time I go back to Bangkok, I notice the same thing: the gap between the people and the system they inhabit. Thais are cosmopolitan, creative, industrious, and increasingly fluent in the language of the global economy. They are also trapped in a structure that was built by a crisis nearly three decades old, maintained by conglomerates whose dominance predates that crisis, and reinforced by a collective memory that treats caution as the highest virtue.

The standard developing-country story is about building human capital. Thailand already has it. The standard demographic decline story is about rich countries running out of young people. Thailand is running out of young people without ever having gotten rich. The standard stagnation story is about countries that can’t attract investment. Thailand attracts plenty of investment. It just flows exclusively into what’s already been validated a hundred times over: another mall, another resort, another 7-Eleven.

None of the usual frames quite fit. And that, more than any single statistic, is what makes Thailand’s situation a tragedy rather than a problem. Problems have known solutions. Tragedies are what happen when the ingredients for success are all present and the structure still won’t let them combine.

The Sathorn Unique still stands downtown. Eighty percent complete. Twenty-seven years empty. Nobody lacks the resources to finish it. They lack the conviction that finishing it is safe.

That’s the frame the crisis installed, and it applies to a lot more than one building.